When the Numbers Lie: Benfords Law and Financial Fraud Detection

When the Numbers Lie: Benford's Law and Financial Fraud Detection

A controller at a mid-size firm has been routing payments to a vendor that doesn't exist. The invoices look clean. The approval chain is intact. The amounts vary enough to stay below internal audit thresholds. Nothing appears wrong.

But the numbers are already confessing.

The first digits of fabricated transactions cluster in ways that legitimate financial activity almost never produces. A trained investigator applying Benford's Law analysis can see the distortion in minutes — long before anyone opens a bank statement or subpoenas a record. The fraudster believes they've covered their tracks. What they don't understand is that the mathematical signature of fabrication is embedded in the very numbers they chose.

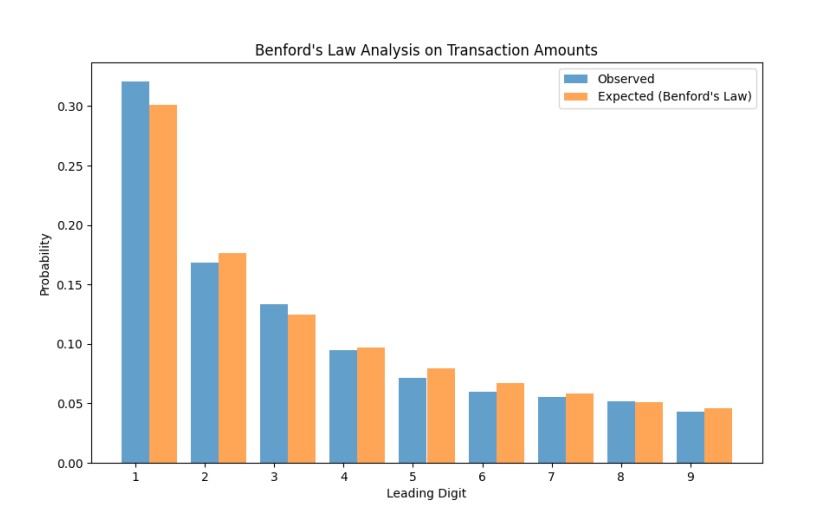

What Benford's Law Actually Reveals

Benford's Law describes the frequency distribution of leading digits in naturally occurring numerical datasets. In datasets that grow organically — revenue figures, transaction volumes, account balances — the digit 1 appears as the first digit roughly 30% of the time. The digit 2 appears about 17.6% of the time. By the time you reach 9, you're down to roughly 4.6%.

Most people assume digits should distribute evenly, around 11% each. That assumption is wrong, and it's precisely what makes Benford's Law effective in financial fraud investigations.

The explanation is logarithmic scaling. A growing financial figure spends more time in lower-digit ranges before crossing into higher ones — more time between $1,000 and $2,000 than between $8,000 and $9,000. When someone fabricates data, they introduce artificial uniformity or clustering that breaks that natural progression. They don't know they're doing it. They just pick numbers that feel plausible.

Why Fraudsters Fail the Benford's Test

People who manipulate financial records are not statisticians. They think in round numbers. They gravitate toward amounts that feel believable — $4,800, $9,500, $7,200 — without understanding that the aggregate pattern of their choices diverges sharply from what authentic financial data looks like.

That's not a theoretical vulnerability. It's an observable, testable, repeatable phenomenon that has held up in courtrooms, regulatory proceedings, and internal corporate investigations for decades. The fraudster's instinct toward psychologically comfortable numbers is the same instinct that exposes them.

How This Works in the Field

Expense and Reimbursement Fraud

An employee submits fabricated expense reports over a two-year period. Each individual claim falls below the approval threshold. The receipts look plausible. But when the first-digit distribution of all submitted amounts is plotted against the Benford curve, the deviation is immediate.

Fabricated expenses tend to cluster around amounts starting with 4, 5, or 7 at frequencies authentic expense data rarely produces. That deviation compresses the investigative aperture from thousands of transactions down to the specific clusters that warrant forensic examination.

Ghost Employee Schemes

A fraudster adds fictitious workers to payroll and routes their compensation to accounts they control. The problem: the fabricated salaries assigned to nonexistent employees rarely mirror the organic distribution of a legitimate payroll dataset.

An abnormal frequency of first digits in the 7, 8, or 9 range across payroll disbursements is a strong indicator — one that points directly toward asset discovery and bank record analysis.

Vendor and Procurement Fraud

This is among the most common schemes we encounter in corporate and tribal government engagements. Shell vendors submit invoices for goods or services never delivered, and the transaction amounts are invented wholesale.

Running vendor payment data through Benford's analysis frequently identifies the fabricated invoices within the first pass — particularly when combined with cross-referencing vendor registration data, payment timing, and entity relationships simultaneously.

Tax Evasion and Government Fund Misallocation

Tax authorities and government oversight bodies have used Benford's Law for years to flag returns and expenditure reports that deviate from expected distributions. For tribal governments navigating federal compliance requirements, this methodology provides an objective, defensible analytical layer when investigating potential misallocation of funds or inflated budget line items — findings that must survive scrutiny from federal oversight agencies.

The Difference Between Forensic Analysis and a Spreadsheet Exercise

Benford's Law is publicly known. The formula is accessible. Anyone with Excel can run a first-digit frequency test. That accessibility is exactly why proper application matters more than awareness of the concept.

A raw Benford's test on the wrong dataset produces noise, not intelligence. Not all financial data conforms to the expected distribution. Datasets with constrained ranges — fixed-price contracts, standardized billing amounts, regulated fee schedules — will deviate from the Benford curve without any fraud present. An inexperienced analyst who doesn't understand these boundary conditions will generate false positives that waste investigative resources and, more importantly, can damage credibility if presented prematurely to opposing counsel or a regulatory body.

At Atlantis, Benford's analysis is one component of a layered investigative methodology that includes:

- Digital forensics through Cellebrite extraction

- Advanced OSINT

- AI-driven pattern recognition through our proprietary MIA platform

- Forensic accounting review

- Targeted witness interviews

The statistical anomaly identified by Benford's analysis becomes actionable only when corroborated through those additional channels.

> Attorneys preparing for litigation need evidence that survives a Daubert challenge — not a chart pulled from an Excel tutorial. The tool is only as valuable as the investigator wielding it.

The Limitations an Honest Investigator Will Tell You About

Any firm that presents Benford's Law as a fraud-detection silver bullet is selling you something. The methodology has real constraints.

Not all deviations indicate fraud. A company that prices most products between $50 and $99 will show elevated frequency of leading 5s through 9s — not because someone is committing fraud, but because the data is structurally constrained. Context determines whether a deviation is suspicious or expected. That judgment comes from experience, not from running the formula.

Sophisticated actors can defeat it. A fraudster who understands Benford's distribution can fabricate numbers that conform to the expected curve. This is uncommon — most financial criminals lack the statistical literacy — but it means Benford's analysis should never be the sole investigative method in any serious matter.

Small datasets are unreliable. Benford's Law requires sufficient data volume to produce statistically meaningful results. Drawing fraud inferences from a dataset of 50 transactions is overreaching. Investigators who do that aren't helping their clients — they're creating exposure.

It identifies where to look, not what happened. Benford's analysis is a triage tool. It narrows the field. The actual determination of fraud requires traditional investigative work: document examination, financial record reconstruction, interviews, and corroborating evidence. The anomaly is the starting point, not the conclusion.

These constraints don't diminish the methodology. They're the reason experienced investigators exist.

When to Commission a Financial Fraud Investigation

The decision to engage typically follows one of several patterns:

- An internal audit has surfaced irregularities that in-house staff cannot explain

- Litigation discovery has produced financial records that require forensic analysis

- A whistleblower has made allegations that demand independent verification

- A fiduciary — corporate, tribal, or familial — suspects that someone in a position of trust is exploiting that position

In every scenario, delay compounds the problem. Financial fraud does not plateau. The longer a scheme operates, the more complex the money trail becomes, the more records are altered or destroyed, and the harder recovery gets.

Atlantis conducts financial fraud investigations for attorneys managing high-value litigation, family offices protecting generational wealth, tribal governments addressing governance failures, and corporate leadership confronting internal misconduct. Our engagement model is built for cases where the stakes preclude a casual approach and the findings must withstand adversarial scrutiny.

If the numbers in your matter don't add up, there's usually a reason. We find it.